Every North Carolinian who pays personal income tax would see a lower rate, under a proposal from legislative Republicans. At the same time, higher-income earners should foot a higher share of the bill.

To understand why, examine the interplay between the state’s flat tax rate and its standard deduction.

North Carolina adopted a “flat tax” in 2013. One tax rate replaced a three-tiered system. The old system’s top rate was 7.75%. Successive tax cuts have placed the current flat rate at 5.25%.

That 32% reduction in the top tax rate makes a difference. Ask businesses and individuals across the country looking at relocation. Still, critics of a flat tax claim it’s unfair that higher earners pay the same tax as those with less income. It’s important to address those concerns.

The name “flat tax” contributes to the problem. The label implies that everyone – rich and poor — pays the same tax. But it’s not a flat dollar amount of tax. It’s a flat tax rate.

With no other deductions or credits, you pay more tax as you earn more money. Under the current rate of 5.25%, a taxpayer making $10,000 would pay $525 in income tax. A taxpayer earning 10 times as much, $100,000, would pay 10 times as much tax: $5,250. A million-dollar earner would owe $52,500. That’s 10 times as much as the $100,000 taxpayer and 100 times as much as the $10,000 earner.

Higher earners clearly pay more. Nonetheless, critics believe high-income taxpayers should cough up a larger percentage of their incomes in taxes. They want North Carolina’s tax system to incorporate some progressivity.

As lawmakers have lowered the flat income tax rate in recent years, they have continually increased the standard deduction. That’s the amount of income removed from the tax man’s consideration.

The current standard deduction is $10,750 for a single filer and $21,500 for a married couple filing jointly.

Use those numbers to revisit the example above. First, consider three single taxpayers at the three contrasting income levels. Rather than pay $525 in income tax, a $10,000 earner actually pays zero income tax. Once the $100,000 earner takes his standard deduction, he owes $4,685. Once the $1 million taxpayer takes his deduction, he pays $51,935.

Use those numbers to revisit the example above. First, consider three single taxpayers at the three contrasting income levels. Rather than pay $525 in income tax, a $10,000 earner actually pays zero income tax. Once the $100,000 earner takes his standard deduction, he owes $4,685. Once the $1 million taxpayer takes his deduction, he pays $51,935.

All three taxpayers benefit from the deduction. But the lower-income earner sees the biggest impact. His entire state income tax burden is wiped away. Meanwhile, the standard deduction knocks about 10% off of the $100,000 earner’s income tax burden. For the $1 million taxpayer, the standard deduction chops 1% off his bill.

The differences are even more pronounced for a married couple. Once again, the $10,000 household pays no income tax. That remains true for couples earning twice as much. Meanwhile, the $100,000 household owes $4,121. The standard deduction cuts more than 21% of its tax bill. The $1 million couple owes $51,371. The standard deduction cuts about 2% of the tax burden.

Before examining changes proposed this year, it’s time for two caveats.

First, the examples above assume taxpayers are taking no other deductions or credits. This is unrealistic. It’s likely that the $1 million earner is itemizing deductions or taking other steps to reduce a state income tax bill of more than $50,000. Even the $100,000 taxpayer is likely to seek more than the standard deduction.

But if other credits and deductions skew the tax code in a way that favors higher earners unfairly, that’s an argument for re-examining those credits. That discussion has no impact on the interplay of a flat tax and standard deduction.

The second caveat involves kids. My examples say nothing about households with children. That’s purposeful. North Carolina’s tax code specifically gears child-related deductions to benefit families with lower incomes. Those deductions generate progressivity in the tax code that has widespread support.

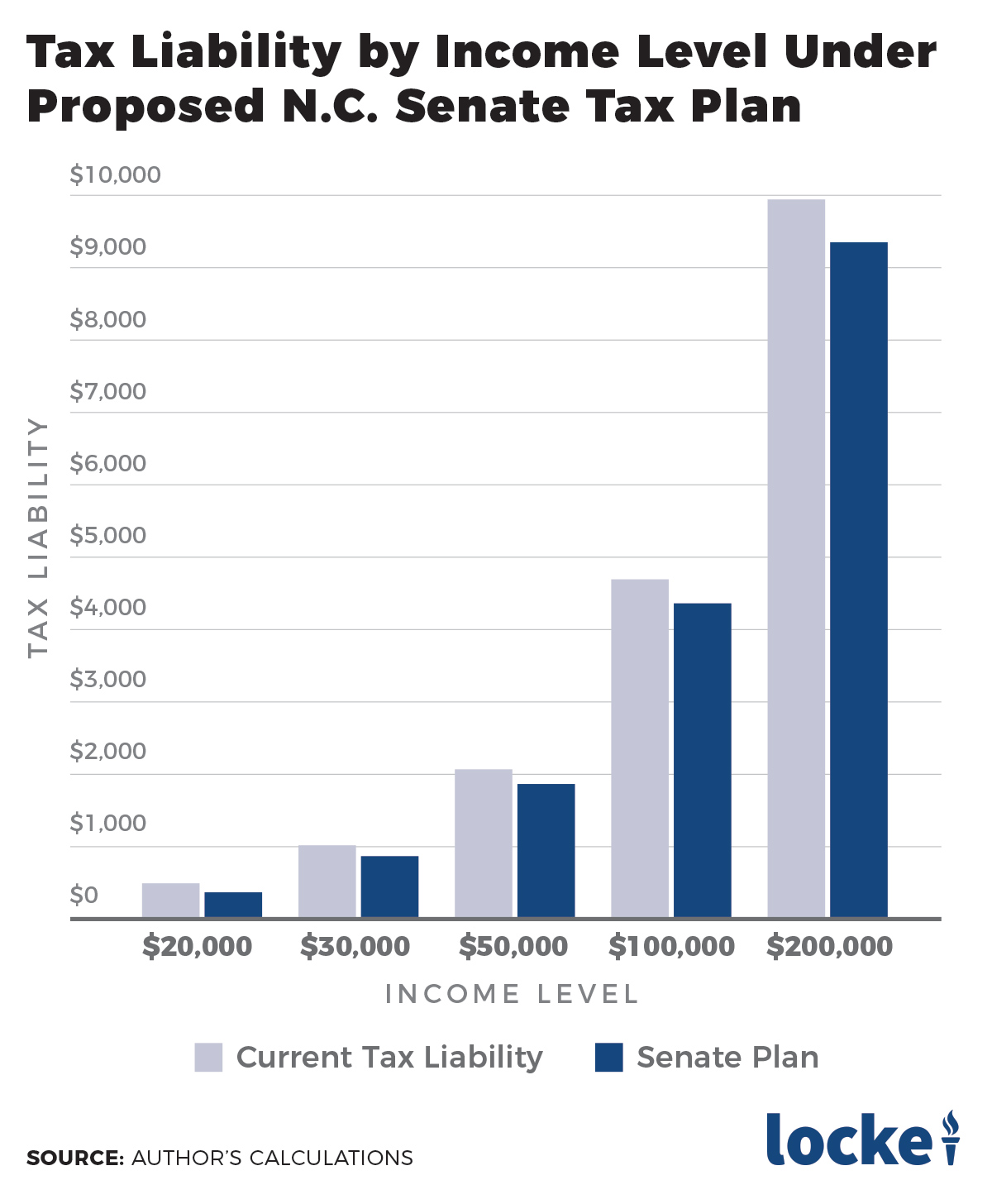

Now, back to this year’s proposals. Senate Republicans have discussed cutting the flat tax rate from 5.25% to 4.99% (a cut of roughly 5%), while boosting the standard deduction from $10,750 to $12,750 (an increase of almost 19%).

Let’s look at prospective changes in income tax bills for single earners with no children making $20,000, $30,000, $50,000, $80,000, $100,000, $200,000, and $1 million.

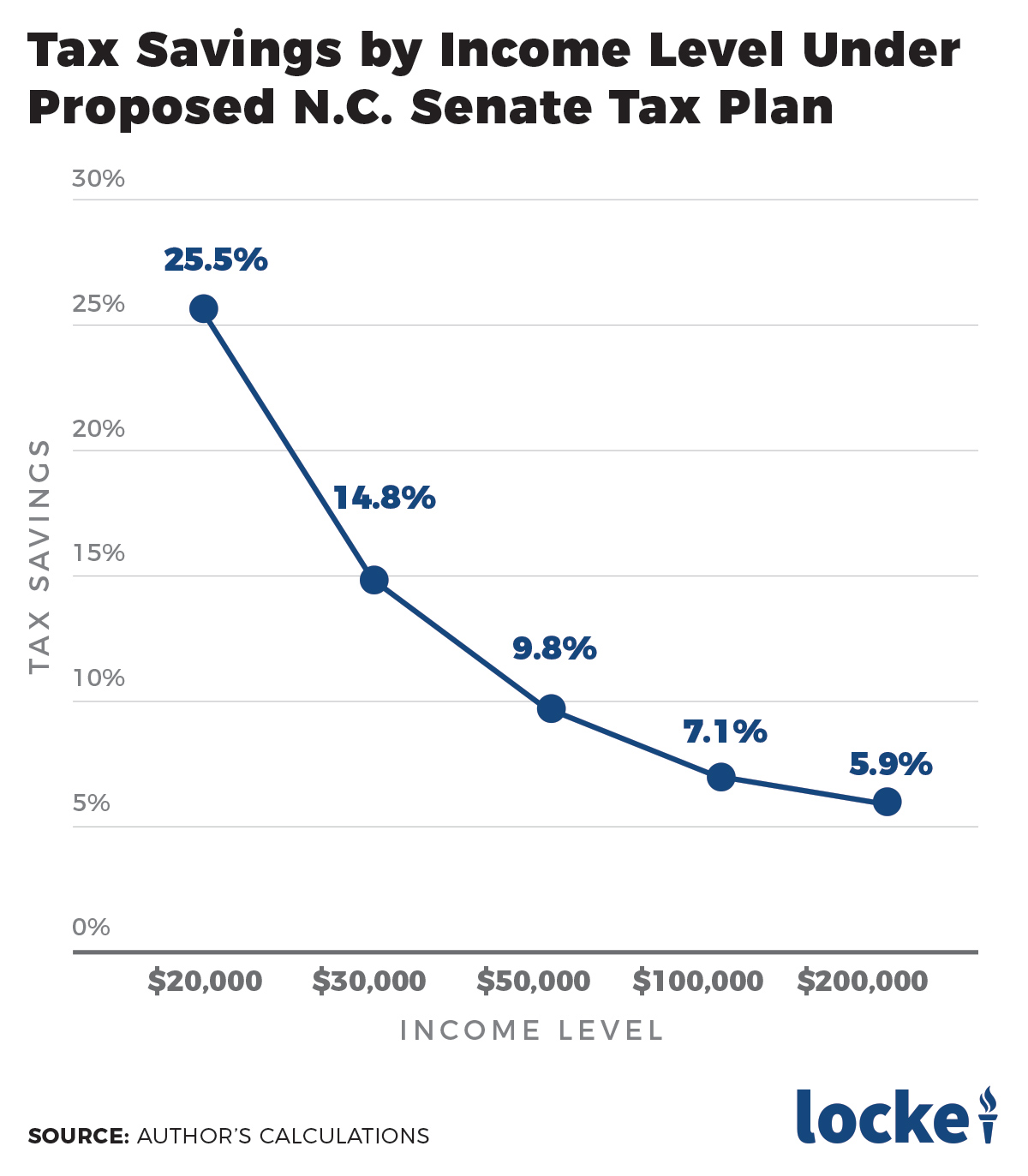

The $20,000 earner would see his income tax bill drop from $485 to $361. That’s a cut of more than 25%. At $30,000, the bill drops from $1,010 to $860 (15% cut). At $50,000, the bill drops from $2,060 to $1,858 (almost 10% cut). At $80,000, the bill drops from $3,635 to $3,355 (8% cut). At $100,000, the bill drops from $4,685 to $4,353 (7% cut). At $200,000, the bill drops from $9,935 to $9,343 (6% cut). At $1 million, the bill drops from $51,935 to $49,263 (5% cut).

The $20,000 earner would see his income tax bill drop from $485 to $361. That’s a cut of more than 25%. At $30,000, the bill drops from $1,010 to $860 (15% cut). At $50,000, the bill drops from $2,060 to $1,858 (almost 10% cut). At $80,000, the bill drops from $3,635 to $3,355 (8% cut). At $100,000, the bill drops from $4,685 to $4,353 (7% cut). At $200,000, the bill drops from $9,935 to $9,343 (6% cut). At $1 million, the bill drops from $51,935 to $49,263 (5% cut).

Note that each taxpayer sees his N.C. income tax bill cut by at least 5%, with earners at the lower end of the income scale seeing larger cuts on a percentage basis. (Repeat this exercise for a married couple, and the lower-income households fare even better.)

It’s also interesting to explore each taxpayer’s relative burden. The $80,000 taxpayer makes four times as much income as the $20,000 taxpayer. Under today’s tax code, he owes 7.5 times as much tax. With the changes, he would owe nine times as much. For the $200,000 taxpayer, who makes 10 times as much as the $20,000 earner, the burden grows from 20 times as much tax liability to 25 times as much.

That’s what happens when lawmakers combine flat tax rate cuts with hikes in the standard deduction. Critics of North Carolina’s system ought to take a closer look.

Mitch Kokai is senior political analyst for the John Locke Foundation.